Housing assistance

Drivers for people seeking housing assistance

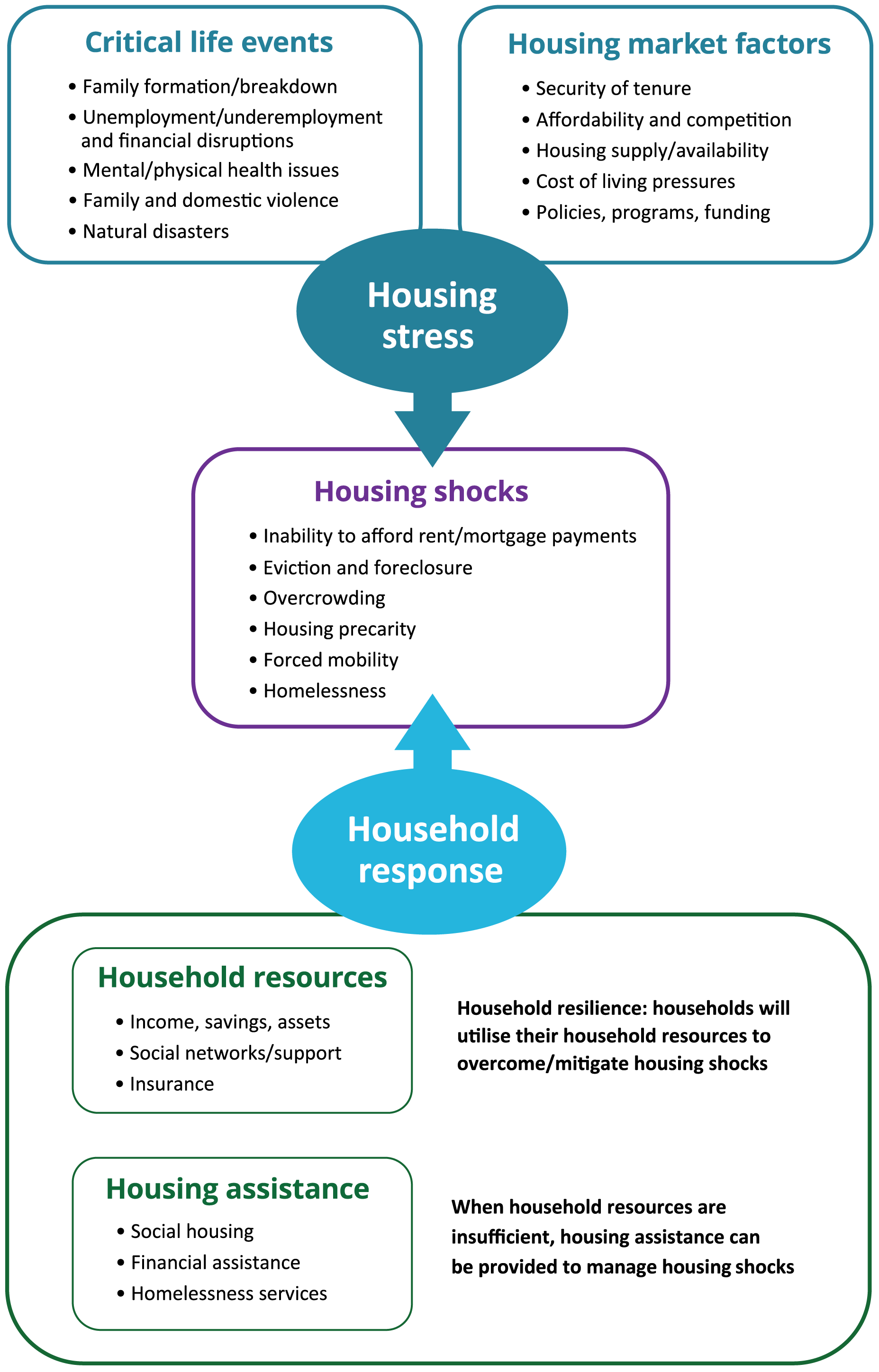

Many circumstances or changes can contribute to the need for people to seek housing assistance. Understanding these drivers, and the influence of critical life events, and housing market factors on households can assist in defining housing stress, an early indicator of household need for housing support. Identifying housing stress can inform interventionist approaches to housing assistance provision and policy (Ghasri et al. 2022).

Housing stress occurs when households pay a high proportion of their income on housing costs. Usually this definition applies to low-income households.

Critical life events can lead to major change in a person’s life. These may include family formation or breakdown, providing care to a family member, loss of a family member, natural disasters, or change of employment. Multiple intersecting critical life events may put significant financial pressure on a household’s ability to manage their housing and living costs.

Housing market factors are the specific arrangement of conditions in the private housing market that impact housing options, and are influenced by:

- taxation

- regulation

- supply

- availability

- low vacancy rates

- rising private market rental costs, and

- cost of living pressures such as inflation, interest rates, and energy costs (Ghasri et al. 2022; Stone et al. 2016).

In response to housing insecurity and housing affordability challenges, households may need to use contingency resources (such as savings, assets, skills, or social networks) to ensure that they can sustain access to housing. However, low-income households often lack the contingency resources to respond to negative impacts arising from critical life events or housing market factors, leading them to seek housing assistance (Ghasri et al. 2022).

Figure 1: Drivers of housing stress