Housing assistance: why do we need it and what supports exist?

Key findings

- Less Australian households own their house outright than ever before, with most households either having a mortgage (36%) or are renting from a private landlord (26%).

- Housing market factors such as housing crisis, inadequate or inappropriate dwelling conditions are one of the main reasons (35%) for clients to seek specialist homelessness services.

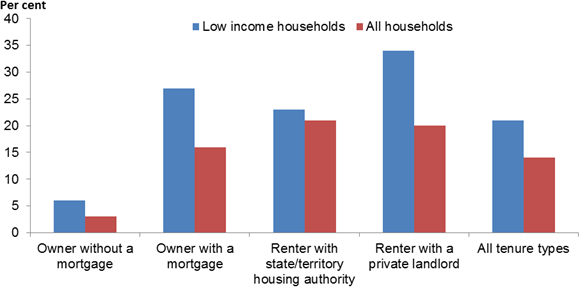

- In 2013–14, low income households were spending 21% of their income directly on housing costs, compared to an average of 14% for all households.

Housing in Australia

Home ownership is a widely held aspiration in Australia, providing security of tenure and long-term social and economic benefits to home owners, though exposing them to some financial risk (AIHW 2013). Having a stable, secure, and suitable place to live is essential to maintaining employment, proper health and nutrition, and improvements in education (AIHW 2014).

In 2013–14, around two thirds (67%) of Australians own their own home (36% with a mortgage and 31% without a mortgage) (ABS 2015).The overall proportion of home ownership has declined by 5% over the last 20 years and the pattern of home ownership has changed. The proportion of households who own their home outright (and do not have a mortgage) has declined (31% down from 42% in 1994–95) whilst households with a mortgage continues to increase (36% up from 30% in 1994-95). The proportion of households renting has also increased over the last 20 years (up from 26% to 31%).

Home ownership can be a major source of wealth but is often a significant source of debt for households. As the proportion of households that have a mortgage or entering the private rental market increases, the proportion of housing costs on their disposable income is also likely to increase. This in particular makes low income households (or those with special needs) vulnerable to housing instability and more likely to require assistance to access and/or maintain appropriate housing.

Drivers for households seeking housing assistance

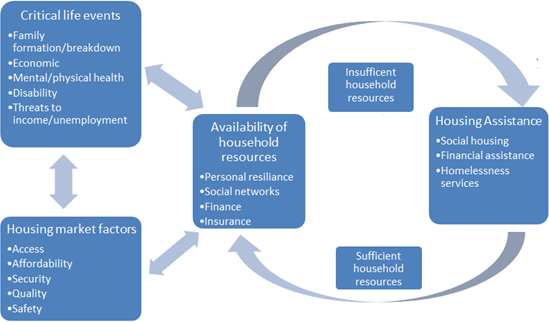

There are many factors that can lead households to seek housing assistance, including critical life events, housing market factors and limited household capacity to manage or avoid the negative impacts of events (Figure 1).

Figure HA.1: Drivers of housing assistance

Source: Adapted from Stone et al. 2015

Critical life events

Critical life events relate to the significant developmental milestones than can occur across the lifespan. Positive critical life events, such as the formation of a family, may lead households to seek housing assistance in their transition to a larger dwelling or a more secure form of housing tenure. Housing assistance also provides a safety net for the more adverse critical life events such as family breakdown, patterns of unemployment or reduction of income, frequent housing transitions, adverse health or loss of loved ones. Research shows that households that experience a number of critical life events which adversely impact on their social and economic circumstances are more likely to need assistance in getting access to housing or maintaining their current housing (Stone et al. 2015).

Family breakdown

Family dissolution and breakdown can often have a negative impact on home ownership or the ability to sustain a tenancy. Changes in the family structure, particularly separations, often increase the costs of housing by increasing housing mobility.

This can result in transitions from home ownership or private rental to precarious housing situations and even homelessness. For example, over half (55%) of all clients seeking specialist homelessness services in 2014-15 reported that they sought assistance due to the breakdown of interpersonal relationships (domestic and family violence and/or relationship/family breakdown) (AIHW 2015c).

Disability

Around 1 in 5 persons in Australia reported living with disability and 1.4 million Australians reported a 'severe or profound core activity limitation' (ABS 2013a). The demand for housing and support services for persons living with disability is expected to increase as Australia's population continues to age (ABS 2013b). The availability of appropriate housing and support services in Australia for people living with disability can often be difficult to access or maintain without additional financial assistance (Wiesel et al. 2015).

Unemployment

The ability to maintain or gain access to housing is closely linked to households having access to stable, regular employment that provides enough to cover housing related costs (mortgage or rental payments) (Stone et al. 2015). Without this stable regular employment, households may find themselves unable to meet rent and mortgage repayments and in urgent need of housing assistance and services.

Housing market factors

Housing market factors that can adversely impact households lead them to seeking housing assistance. Adverse housing market factors include the inability to maintain current housing costs or limited access to affordable housing (housing affordability), conflict with landlords, inappropriate housing conditions, difficulty securing new tenancies, and unwanted or frequent housing mobility (Stone et al. 2015). There is a strong relationship between these issues and homelessness. For example, in 2014–15, one in three clients (35%) of specialist homelessness services reported accommodation issues (e.g. housing crisis, inadequate or inappropriate dwelling conditions, previous accommodation ended) as their main reason for seeking assistance (AIHW 2015c).

Housing affordability and stress

In recent years, house prices have risen significantly, at a higher rate than consumer prices and median incomes, impacting housing affordability (AIHW 2014). Housing affordability refers to a person's ability to meet costs associated with housing, based on their income. An increasing lack of affordable housing puts households at an increased risk of experiencing housing stress, and could be forced into decisions that will adversely affect them. Housing stress does not only have financial impacts. It can result in an exacerbation of stress-related health conditions, increased relationship stresses, going without meals, restricted extracurricular activities for children and an inability to afford additional housing expenses (such as property maintenance) (Yates & Milligan 2007).

Research has shown housing stress to exist in owner occupied and private rental tenures (Jacobs et al. 2010). Housing stress is less common in social housing as rent setting policies ensure that tenants do not pay more than 30% of their income on housing costs. A common measure of housing stress is where a household's housing costs, primarily mortgage repayments or rents, exceed 30% of their gross income (ABS 2015). Both purchasers and renters can be in housing stress. As households on higher incomes may choose to spend more of their income on housing, the 30% measure is a better indicator of low-income households (the bottom 40%) who are likely to be struggling with housing costs (AIHW 2015b).

Figure HA.2 shows that in 2013–14, low income households were spending 21% of their income directly on housing costs, compared to an average of 14% for all households (ABS 2015). Housing costs as a proportion of income were the highest for lower income households renting with a private landlord (34%).

Figure HA.2: Average housing costs as a proportion of income by tenure type, 2013–14

Notes:

- Housing costs are mortgage repayments, rent and rate payments (general and water)

- Percentile measures are within the equivalised income distribution

- Low income households include the lowest and second equivalised disposable household income quintiles, excluding the 1st and 2nd percentiles (i.e. the 3rd to 40th percentiles inclusive). The 1st and 2nd percentiles are excluded due to the high wealth and expenditure characteristics those household exhibit, and the prevalence of income types other than employee income and government pensions and allowances.

Source: ABS 2015

Lack of household resources

Households that experience a critical life event or are impacted by housing market factors, rely on the household resources (such as savings, insurances, social networks) to ensure that they are able to access or sustain appropriate housing (Stone et al. 2015). Households with low incomes often lack the resources to insure against any negative impacts arising from critical life events and/or housing market factors leading them to require housing assistance (Figure HA.1).

Housing assistance can provide a safety net when costs associated with accessing or maintaining housing are not able to be met by the household. Housing assistance can be short term or long term and can vary depending on the needs of the individual and/or household. Housing assistance is generally provided through provision of subsidised rental housing (social housing), financial payments (e.g. Commonwealth Rent Assistance) and/or specialised homelessness services.

Housing assistance policy framework

On 1 January 2009, The National Affordable Housing Agreement (NAHA) took effect, and provides a broad framework for the Australian and State and Territory Governments to improve housing outcomes in all tenure types, as well as to reduce homelessness (SCRGSP 2016).

The NAHA aims to ensure 'all Australians have access to affordable, safe and sustainable housing that contributes to social and economic participation' (COAG 2009, p3). Under the NAHA, governments have committed to undertake a range of reforms that will improve housing affordability including:

- improved integration and coordination of assistance to people who are homeless or at risk of homelessness;

- improvements to social housing arrangements to reduce concentrations of disadvantage and improve the efficiency of social housing;

- improving access by Indigenous people to mainstream housing, including home ownership and contributing to the 'Closing the Gap' targets; and

- other reforms to increase the supply of affordable housing.

The NAHA provides the framework for all levels of government to work together into the future to improve housing affordability for low and moderate income households (COAG 2009).

Housing assistance programs

Housing assistance interventions provided by Australian governments not only aim to meet housing needs, they also contribute to improved social and economic well-being for individuals, as well as families and communities.

Housing assistance in Australia is provided in many forms, including:

- Social housing—provided by not for-profit, non-government or government organisations that provide eligible households housing with rents set below market rates (based on a percentage of a tenants income). Forms of social housing include public housing (PH), state owned and managed Indigenous housing (SOMIH), community housing (CH), and Indigenous community housing (ICH).

- Commonwealth Rent Assistance (CRA)—a non-taxable income support supplement payable to people who: rent in the private market or community housing; receive an income support payment or more than the base rate of Family Tax Benefit part A; and pay rent above a minimum threshold.

- Private Rent Assistance (PRA)—a financial assistance provided by state and territory governments to low-income households experiencing difficulty in securing or maintaining private rental accommodation. Types of assistance include bond loans, rental grants, subsidies and relief, and relocation expenses.

- First Home Owner Grant (FHOG)—a one-off grant payable to low-income first home owners who satisfy eligibility criteria. This was introduced on 1 July 2000 and is funded by the states and territories (where the FHOG is still available) and administered under their own legislation.

- Home Purchase Assistance (HPA)—a range of financial assistance to eligible households to improve their access to, and maintain, home ownership. This is administered by each jurisdiction.

In 2014–15, the Australian Government provided $1.9 billion to state and territory governments to deliver housing assistance under the NAHA, and $4.2 billion for CRA (SCRGSP 2016).

Governments across Australia also fund a range of services to support people who are homeless or at risk of homelessness, known as Specialist Homelessness Services (SHS). These services are delivered by non-government organisations including agencies specialising in delivering services to specific target groups (such as young people or people escaping domestic violence), as well as those that provide more generic services to those facing housing crises. (AIHW 2015c). This includes circumstances where social housing tenants may require assistance from specialist homelessness services to maintain their social housing tenancy (AIHW 2015a). The type of support offered to those in social housing is generally through case management and support services compared to financial assistance for those in private rental (Stone et al. 2015).

Across Australia, a range of options for people with disabilities who require housing support are also available. The National Disability Insurance Scheme (NDIS) has the capacity to provide access to services supporting those with disability to live independently including home modifications, and support with personal and domestic care (NDIS 2014).

References

Australian Bureau of Statistics (ABS) 2013a. Disability, ageing and carers, Australia: summary of findings 2012. ABS cat no. 4430.0, Canberra ABS.

ABS 2013b. Population projections, Australia, 2012 (base) to 2101. ABS cat no. 3222.0, Canberra: ABS.

ABS 2015. Housing Occupancy and Costs, 2013–14. ABS cat no. 4130.0, Canberra: ABS.

Australian Institute of Health and Welfare (AIHW) 2013. Housing Assistance in Australia 2013. Cat. no. HOU 271. Canberra : AIHW.

AIHW 2014. Housing Assistance in Australia 2014. Cat. no. HOU 275. Canberra : AIHW.

AIHW 2015a. Exploring transitions between homelessness and public housing: 1 July 2011 to 30 June 2013. Cat no. HOU 277. Canberra: AIHW.

AIHW 2015b. Housing assistance in Australia, Canberra: AIHW. Viewed 7 March 2016.

AIHW 2015c. Specialist homelessness services report 2014–15, Canberra: AIHW. Viewed 8 March 2016.

Council of Australian Governments (COAG) 2009. National Affordable Housing Agreement: Intergovernmental Agreement on Federal Financial Relations. Canberra: COAG. Viewed 18 February 2016.

Jacobs K, Atkinson R, Spinney A, Colic-Peisker V, Berry M & Dalton T 2010. What future for public housing? A critical analysis. Melbourne: AHURI.

National Disability Insurance Scheme (NDIS), 2014. Mainstream interface: Housing and independent living, Fact Sheet, Canberra: NDIS. Viewed 3 March 2016.

SCRGSP (Steering Committee for the Review of Government Service Provision) 2016. Report on government services 2016. Canberra: PC.

Stone W, Sharam A, Wiesel I, Ralston L, Markkanen S, James A, 2015. Accessing and sustaining private rental tenancies: critical life events, housing shocks and insurances, AHURI Final Report No.259. Melbourne: Australian Housing and Urban Research Institute Limited. Viewed 8 March 2016.

Wiesel I, Laragy C, Gendera S, Fisher K R, Jenkinson S, Hill T, Finch K, Shaw, W. & Bridge C, 2015. Moving to my home: housing aspirations, transitions and outcomes of people with disability, AHURI Final Report No.246. Melbourne: Australian Housing and Urban Research Institute. Viewed 8 March 2016.

Yates J 2011. Explaining Australia's trends in home ownership. Housing Finance International, Winter:6-13.

Yates J & Milligan V. 2007. Housing affordability: a 21st century problem. Final report no. 105. Melbourne: AHURI.