Clients, services and outcomes

Specialist homelessness agencies provide a wide range of services to assist those who are experiencing homelessness or who are at risk of homelessness, ranging from general support and assistance to immediate crisis accommodation. Characteristics of all clients assisted by specialist homelessness services (SHS) in 2018–19 are described below, including their needs for assistance and the services they received.

Key findings

- More than 1.2 million clients have been assisted by SHS agencies since the collection began in 2011–12.

- More than half (57%) of all clients in 2018–19 had previously been assisted by a SHS agency at some point since the collection began in 2011–12.

- In 2018–19, around 290,300 clients sought assistance from SHS agencies, equating to 116.2 clients per 10,000 population.

- In 2018–19, almost 181,900 clients (63%) were formally referred to a specialist homelessness agency, most commonly from another specialist homelessness agency or outreach worker (14%), other agency (government or non-government) (11%) or by the police (6%).

- Upon first presentation, most clients seeking assistance were housed but at risk of homelessness (58% or 153,700); of these, most were living in private or other housing (61% or 93,800) or public or community housing at the time (23% or 35,700).

- 3 in 10 SHS clients (30%) received accommodation in 2018–19 and the median length of accommodation was 29 nights.

- 4 in 10 clients were homeless on presentation to a SHS agency. Of these, agencies assisted about 38% into housing, most into private or other housing (about 16,500) and a further 10,400 into public or community housing.

- SHS agencies assisted more than 8 in 10 clients who were in private or other housing (85% or 59,200 clients) and public or community housing (86% or 22,600 clients) at the beginning of support to maintain their tenancy at the end of support.

- The average amount of financial assistance provided totalled $874 per client, up from $794 in 2017–18 (not adjusted for inflation).

SHS clients at a glance

The estimated number of clients assisted by specialist homelessness agencies increased from 255,700 in 2014–15 to 290,300 in 2018–19; an average annual increase of 3.2%. The rate of SHS clients increased from 108.9 clients per 10,000 population in 2014–15 to 116.2 clients in 2018–19 (Table CLIENTS.1).

It is important to note, the Specialist Homelessness Services Collection (SHSC) data provide a measure of service response. Increases in client numbers reflect an increase in agency engagement of people which may be due to an increase in availability and accessibility of services or the utilisation of these services, not necessarily a change in the underlying level of homelessness in Australia.

Housing situation at the beginning of the first support period (proportion (per cent) of all clients) | |||||

|---|---|---|---|---|---|

2014–15 | 2015–16 | 2016–17 | 2017–18 | 2018–19 | |

Number of clients | 255,657 | 279,196 | 288,273 | 288,795 | 290,317 |

Rate (per 10,000 population) | 108.9 | 117.2 | 119.2 | 117.4 | 116.2 |

Homeless | 43 | 44 | 44 | 43 | 42 |

At risk of homelessness | 57 | 56 | 56 | 57 | 58 |

Total days of support (millions) | 19.7 | 22.2 | 23.4 | 24.7 | 26.0 |

Length of support | 33 | 35 | 37 | 39 | 44 |

Proportion receiving accommodation | 33 | 31 | 30 | 29 | 30 |

Total nights of accommodation (millions) | 6.6 | 7.0 | 6.9 | 6.9 | 7.0 |

Median number of nights accommodated | 34 | 33 | 33 | 32 | 29 |

Achievement of all case management goals (per cent) | 26 | 23 | 23 | 24 | 25 |

Notes

- Rates are crude rates based on the Australian estimated resident population (ERP) at 30 June of the reference year. Minor adjustments in rates may occur between publications reflecting revision of the estimated resident population by the Australian Bureau of Statistics.

- The denominator for the proportion receiving accommodation is all SHS clients. Denominator values for proportions are provided in the relevant supplementary table.

- The denominator for the proportion achieving all case management goals is the number of client groups with a case management plan. Denominator values for proportions are provided in the relevant supplementary table.

- Data for 2014–15 to 2016–17 have been adjusted for non-response. Due to improvements in the rates of agency participation and SLK validity, data from 2017–18 are not weighted. The removal of weighting does not constitute a break in time series and weighted data from 2014–15 to 2016–17 are comparable with unweighted data for 2017–18 onwards. For further information, please refer to the Technical notes.

Source: Specialist Homelessness Services Collection 2014–15 to 2018–19.

Characteristics of clients

43% of SHS clients in 2018–19 were first time clients (since the collection began in 2011–12).

The characteristics of clients, the main reasons for seeking assistance, and the services that had been supplied to clients, have remained relatively stable over the 5 years to 2018–19 (Table CLIENTS.1). The top changes over time include:

- Length of support has increased with the median number of days a client was supported increasing from 33 days in 2014–15 to 44 days in 2018–19.

- In 2018–19, the number of females presenting homeless (58,700) was higher than the number of males (53,300), up from 49,800 females and 48,700 males in 2014–15.

- The number of clients aged 65 and over are a growing group receiving SHS; up from 6,400 (3% of SHS clients) in 2014–15 to almost 8,500 (3%) in 2018–19.

- The housing outcomes for SHS clients presenting homeless have been changing; in 2014–15, similar numbers of these clients were housed in either public or community housing, or private or other housing at the end of support (9,800 and 13,000 respectively). In 2018–19, the number of clients in this group assisted into housing has grown to almost 28,000 with 6 in 10 (or more than 16,500) housed in private or other housing.

Age and sex

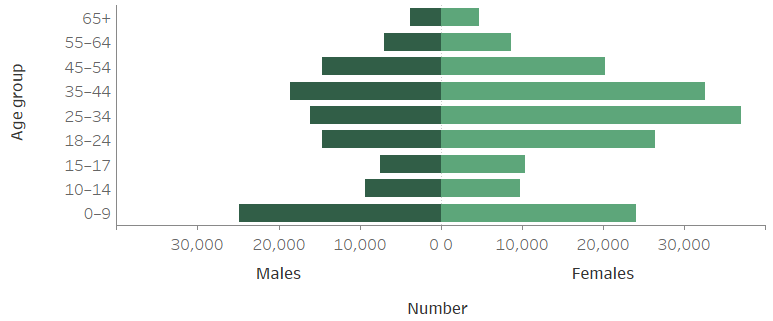

Figure CLIENTS.1 illustrates the age and sex distribution of SHS clients in 2018–19:

- The majority of clients were female (60% or more than 173,600 clients).

- The proportion of males (50% of males) who were experiencing homelessness at the start of support was higher than females (37%).

- 3 in 10 clients were aged under 18 (30% or almost 85,800).

- 1 in 6 were children under the age of 10 (17% or more than 48,900 clients).

- Among adult clients, the largest age group was those aged 25–34, accounting for almost 1 in 5 clients (18%), most of whom were female.

- The most common age group for males was those aged 0–9 years (21%) while for females, the most common age group was 25–34 (21%).

- The overall rate of service use was higher for females: 1 in 73 females in the Australian population received specialist homelessness services compared with 1 in 106 males.

Figure CLIENTS.1: Clients by age and sex, 2018–19

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.1.

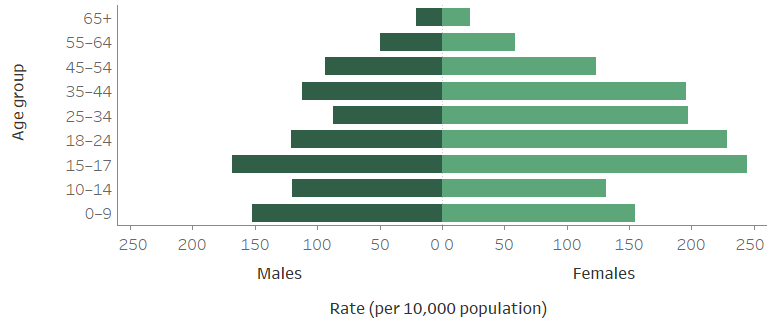

Figure CLIENTS.2 illustrates the rate of service use of SHS clients by age in 2018–19:

- The highest rate of clients were those aged 15–17 years: higher for females (244.4 per 10,000 population) than for males (167.8).

- The lowest rate of clients was for those aged 65 and over (22 per 10,000 population): again higher for females (22.5 per 10,000 population) than males (20.7).

Figure CLIENTS.2: Clients per 10,000 population, by age and sex, 2018–19

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.1.

Indigenous status

In 2018–19, Aboriginal and Torres Strait Islander people continued to be over-represented among SHS clients with more than one-quarter of clients (26% or almost 68,900) who provided information on their Indigenous status identifying as being of Aboriginal and/or Torres Strait Islander origin. Nationally, this equated to 832 Indigenous clients per 10,000 Indigenous population compared with a rate of 85 for non-Indigenous clients.

For further information about Indigenous clients please see Indigenous clients.

State and territory of clients

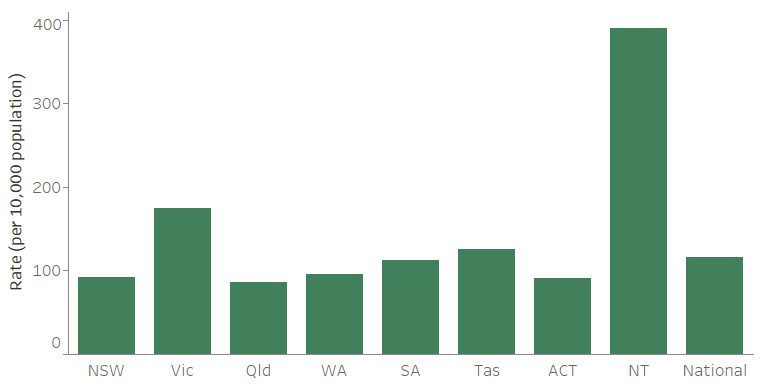

The largest number of clients accessed services in Victoria (112,900), followed by New South Wales (73,500) and Queensland (43,100) (Supplementary table CLIENTS.1), noting that clients may have accessed services in more than one state or territory.

- The highest rate of SHS clients was in the Northern Territory where there were 390 clients per 10,000 population, followed by Victoria (175) and Tasmania (125) (Figure CLIENTS.3).

- Females had higher rates of service use than males across all states and territories; the Northern Territory had the most pronounced difference between males and females where 515 per 10,000 females received services compared with 274 per 10,000 males (Supplementary table CLIENTS.1).

- Overall, more than half of clients in 2018–19 had received services at some point since the collection began in 2011–12. The proportion of returning clients varied across jurisdictions with South Australia reporting the highest proportion (63%) and New South Wales the lowest (53%).

- Nationally, 26.0 million support days were provided in 2018–19; an increase of more than 1.3 million days since 2017–18. Support provided by services in Victoria were responsible for the major share of the increase in support days (an increase of almost half a million days), however Queensland reported the greatest change, up 10% since the previous reporting period.

Figure CLIENTS.3: Client per 10,000 population, by state and territory, 2018–19

Note: Rates are crude rates as detailed in Technical information.

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.1.

Country of birth

Most clients of specialist homelessness agencies in 2018–19 were born in Australia; almost 9 in 10 clients (86% or 215,000) (Supplementary table CLIENTS.2). This proportion is higher than the general Australian population, of whom 71% were born in Australia (ABS 2019). Of those clients who reported their country of birth and were born overseas, the most common country of birth was New Zealand (2%) (Supplementary table CLIENTS.3). Over half of the clients (55%) who were born overseas had arrived in Australia prior to 2009 (Supplementary table CLIENTS.4). Almost 9 in 10 (87% or over 32,100) clients who were born overseas lived in Major cities (Supplementary table CLIENTS.5).

Living arrangements

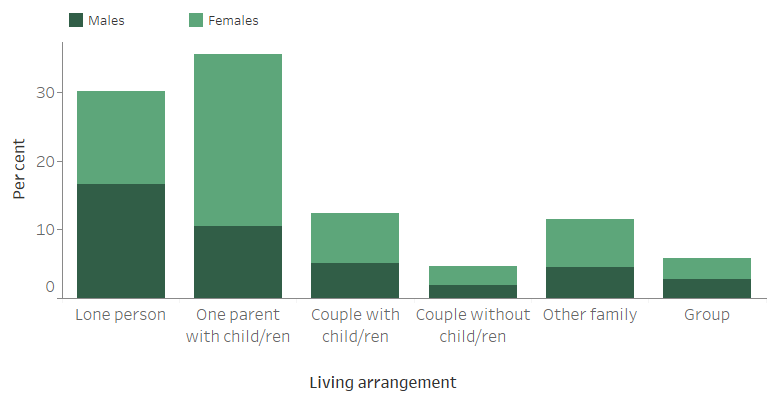

Living alone may be a sign of social advantage or disadvantage (De Vaus and Qu 2015). For some, it is associated with lower income, low participation in the labour force and lower levels of education. Living alone has also been shown to be a risk factor for social isolation (AIHW 2017). With limited economic resources and social networks, lone persons may be more vulnerable to homelessness. By way of comparison, according to the 2016 Census results, overall in Australia, 24% of households consist of a lone person, with most households having families or groups (76%) (ABS 2017).

The most common living arrangement reported by clients at the beginning of support in 2018–19 was lone parent with 1 or more children (36% or around 95,700), followed by lone persons (30% or around 81,300) and couples with 1 or more children (12% or around 33,400) (Figure CLIENTS.4). Female clients were more likely than male clients to be living as a single parent with 1 or more children (43% females compared with 25% males) while males were more likely than females to be living alone (40% males compared with 23% females).

Figure CLIENTS.4: Clients, by living arrangement, 2018–19

Notes

- This data item indicates the group of people with whom the client lives.

- Per cent calculations based on total clients, excluding ‘Not stated’.

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.7.

Housing situation

Among those clients whose detailed housing status was known at the beginning of their first support period in 2018–19:

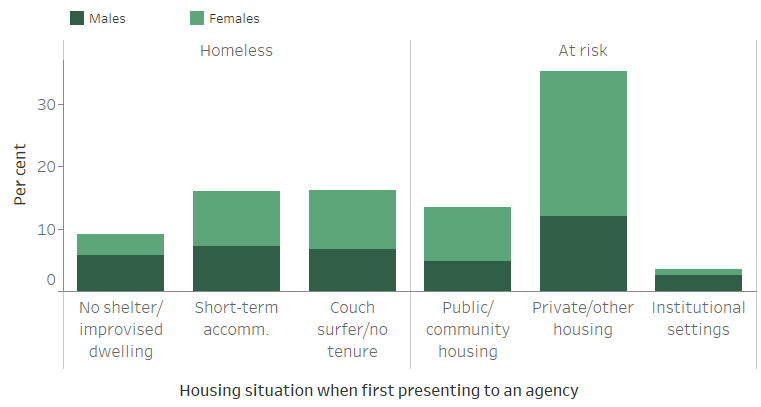

- Most (58% or more than 153,700 clients) were at risk of homelessness and 42% (more than 112,000 clients) were homeless (Figure CLIENTS.5).

- More than 1 in 3 clients (35% or more than 93,800) were living in private or other housing (renter, rent-free, or owner) when presenting to agencies for assistance.

- Of those clients with no shelter/improvised dwelling (more than 24,400 clients), 46% were sleeping in no dwelling, either on the street, in a park or out in the open and a further 22% (1 in 5) were sleeping in a car.

Figure CLIENTS.5: Clients by housing situation at the beginning of support, 2018–19

Notes

- Per cent calculations based on total clients, excluding ‘Not stated’.

- Housing situation ‘Other’ not shown.

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.8.

Main source of income

Income support was high among SHS clients with 78% of clients aged 15 and over receiving some form of government payment as their main source of income at the time they sought support in 2018–19 (Supplementary table CLIENTS.12). The most common government payments were Newstart Allowance (30% or about 57,000 clients), Parenting Payment (18% or 34,500) and Disability Support Pension (15% or 29,500). A total of 9% reported income from employment as their main source and 9% reported having no income.

Education

Of those whose educational status was known, over half of young people aged 5–24 (54% or over 48,100) were enrolled in some form of education in 2018–19 (Supplementary table CLIENTS.13). Almost 9 in 10 (88%) clients aged 5–14 were enrolled in school, 12% of clients aged 5–14 (about 4,500) were not enrolled in education. Almost 7 in 10 (69%) clients aged 15–24 were not in some form of education (around 36,200 clients).

Labour force

Almost 73,300 (38%) clients were not in the labour force in 2018–19 (Supplementary table CLIENTS.14). Over 92,900 (49%) clients aged 15 or over were unemployed at the beginning of support. Males (55%) were more likely to be unemployed than females (45%). More than 1 in 10 (13%) clients were employed and of these, around 3 in 5 (61%) were employed on a part-time basis.

Clients service use in 2018–19

Support periods

Data collected by specialist homelessness agencies are based on support periods or episodes of assistance provided to clients (see Technical notes for further information). Clients may have had more than 1 support period in 2018–19, either with the same agency at different times or with different agencies.

- In 2018–19, clients assisted by homelessness agencies had almost 509,700 support periods. The number of support periods has increased by an average annual growth of 4.0% each year since 2011–12 (Supplementary table CLIENTS.1 and Historical table 1).

- Two-thirds of clients in 2018–19 had only 1 support period (66%) while 1 in 5 (19%) had 2 support periods, 7% had 3 periods and 8% had 4 or more. The average number of support periods per client was consistent with 2017–18 (1.8 support periods per client) (Supplementary table CLIENTS.21).

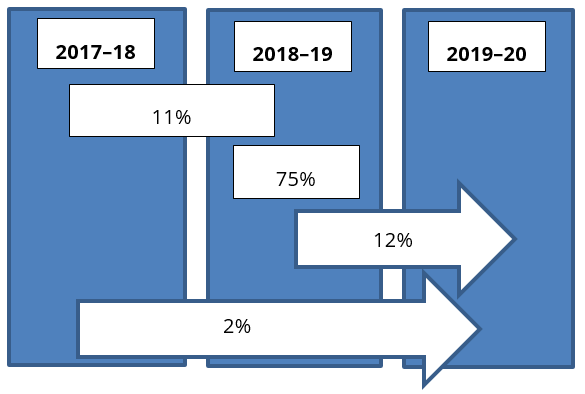

- The majority of support periods were opened and closed within 2018–19 (75% or around 383,100). An additional 12% of support periods opened during the year and remained open on 30 June 2019. Just 2% were ongoing throughout the 2018–19 reporting period (Figure CLIENTS.6).

Figure CLIENTS.6: Support periods, by indicative duration over the reporting period, 2018–19

Number of days clients received support

26.0 million support days were provided in 2018–19.

- In 2018–19, the median number of support days for all clients was 44 days, while clients were supported for an average of 89 support days in total, either as consecutive days or over multiple support periods (Supplementary table CLIENTS.23).

- Males (43 days) and females (45 days) received a similar median length of support.

- The needs of some clients can be met relatively quickly but clients with more complex needs received more support. Around 3 in 10 clients (29% or about 83,400) received between 6 and 45 days of support during 2018–19, while 22% received support for up to 5 days. Seventeen per cent received over 180 days of support; while 16% received support for 91–180 days.

Reasons that support ended

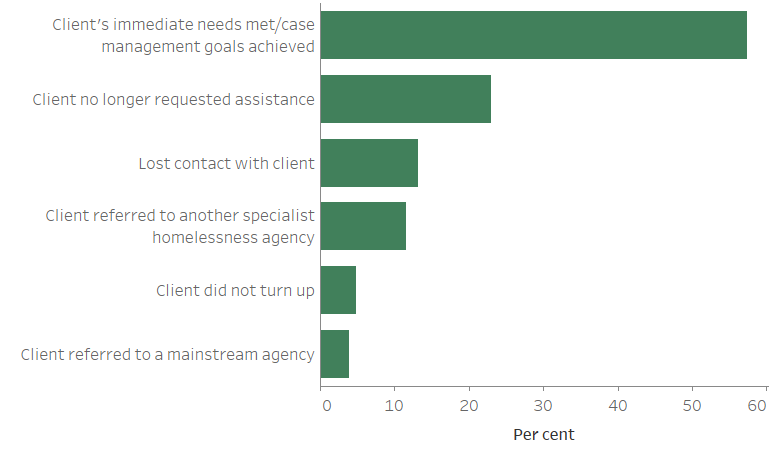

- More than half (57%) of support periods ended in 2018–19 because the client’s immediate needs were met or case management goals were achieved.

- Almost one-quarter (23%) of support periods ended because the client no longer requested assistance; that is, a client may have decided that they no longer required assistance or they may have moved from the state/territory or region.

- A further 12% of support periods closed because the client was referred to another specialist homelessness agency and 13% closed because contact was lost with the client (Figure CLIENTS.7).

Figure CLIENTS.7: Clients by reason support period ended (top 6), 2018–19

Notes

- Top 6 excludes 'Other' reason and cases where reason 'Not stated'.

- Includes clients with any closed support at the end of the reporting period.

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.24.

Clients’ needs for assistance and services provided

The SHSC includes information about clients’ needs for services from two perspectives:

- The client’s reasons for seeking assistance at the start of support – both the main reason for seeking support and all reasons for seeking support are collected.

- The agency worker’s assessment of the client’s needs – this information is captured when clients first present for assistance and each month while a client is still in contact with the agency.

Technical notes and Glossary provide more information about how clients’ needs for assistance are captured in the SHSC.

Services provided to clients range from the direct provision of accommodation, such as a bed in a shelter, to more specialised services such as counselling and legal support. These services are generally either provided to the client directly by the agency or the client is referred to another service. Unmet need provides further information about clients’ needs that went unmet.

Reasons for seeking assistance

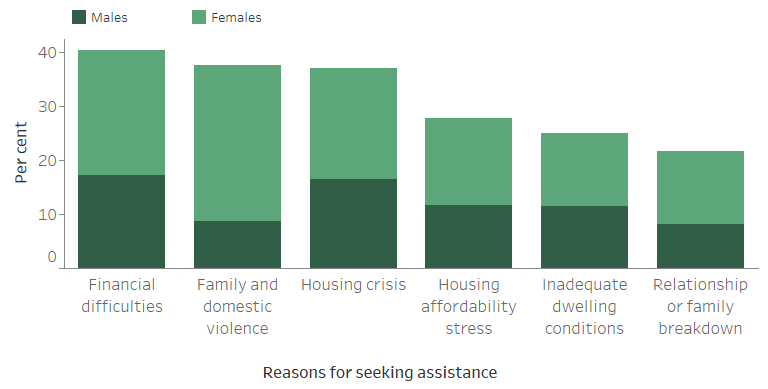

SHS clients can identify a number of reasons for seeking assistance, reflecting the range of situations that contribute to housing instability (Figure CLIENTS.8):

- Accommodation issues (including housing crisis, inadequate or inappropriate dwelling conditions and that previous accommodation had ended) were nominated as a reason for seeking help in over half of all clients; identified by 53% of clients (or around 153,400 clients), similar to previous years.

- More than one-third (37% of clients) were experiencing housing crisis.

- A higher proportion were experiencing financial difficulties, identified by 41% of clients, while over 1 in 4 clients were affected by housing affordability stress (28%).

- Interpersonal and relationship issues, including family and domestic violence, affected over half of all SHS clients; 52% of all clients (about 150,000) identified interpersonal relationships as a reason for seeking support. Within this group, 38% identified family and domestic violence.

Figure CLIENTS.8: Clients by all reasons for seeking assistance (top 6), 2018–19

Note: Top 6 excludes ‘Other’ reason and cases where reason 'Not stated'.

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.15.

While clients can identify a number of reasons for seeking assistance from SHS, agencies also record the main reason for seeking assistance:

- Family and domestic violence was the most common main reason identified for seeking assistance for almost 1 in 3 clients (28% or about 80,500) (Figure CLIENTS.9). For more information, see Clients experiencing family and domestic violence.

- 1 in 5 (20%) identified housing crisis as the main reason for seeking assistance.

Figure CLIENTS.9: Clients by main reason for seeking assistance (top 6), 2018–19

Note: Top 6 excludes ‘Other’ reason and cases where reason 'Not stated'.

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.16.

For those clients presenting at risk of homelessness, the most common main reasons for seeking assistance were (Supplementary table CLIENTS.17):

- family and domestic violence (32%)

- housing crisis (17%)

- financial difficulties (15%).

For those clients presenting as homeless, the most common main reasons for seeking assistance were:

- housing crisis (26%)

- family and domestic violence (18%)

- inadequate or inappropriate dwelling conditions (17%).

General support and assistance

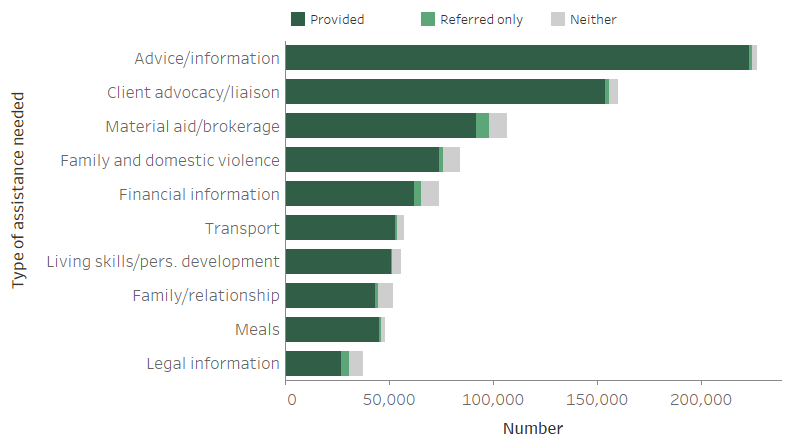

Some types of assistance provided by SHS agencies can be described as ‘general support and assistance’, compared with more specialised services. These services include advice and information, material aid, meals and living skills. In 2018–19:

- Clients most commonly need advice and information, needed by 78% of clients (over 227,300). The next most common need was advocacy and liaison, needed by 55% of clients (almost 160,200) and material aid/brokerage which was needed by 37% of clients (more than 106,900) (Figure CLIENTS.10).

- Services almost always provided the required advice and information. This differs from some specialised services, such as legal information and training or employment assistance, for which clients were more often referred to another agency (see Supplementary table CLIENTS.18).

- Clients needing assistance for family and domestic violence services decreased. In 2018–19, there were about 7,500 less clients (or 8% decrease) requesting assistance for family and domestic violence compared with the previous year.

Figure CLIENTS.10: Clients by need for general services and service provision status (top 10), 2018–19

Notes

- Top 10 excludes ‘Other basic assistance’.

- ‘Neither’ indicates a service was neither provided nor referred.

- The general services group is a count of unique clients within all categories in the service and assistance group. A client may request multiple services and assistance types, therefore the sum of the categories is not equal to the group total.

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.18.

Housing and accommodation services

Housing and accommodation services provided by agencies include:

- short-term or emergency accommodation

- medium-term/transitional housing

- long-term housing

- assistance to sustain tenancy or prevent tenancy failure or eviction

- assistance to prevent foreclosures or for mortgage arrears.

There were over 6,400 more clients (a 4% rise) requesting accommodation services compared with 2017–18.

In 2018–19, 58% of SHS clients identified a need for accommodation services. Of these nearly 169,200 clients:

- 86,100 (51%) were provided with accommodation by the agency

- 25,800 (15%) were referred to another agency for accommodation provision

- 57,200 (34%) were neither provided nor referred for assistance. These clients are further described in Unmet need.

Assistance to sustain tenancy/prevent eviction was needed by 34% of clients at some stage during their support in 2018–19, a similar proportion to the previous year. This group includes those who were still housed when they approached a SHS agency and were supported to remain in that housing. It also includes those who identified a need for accommodation, were assisted to secure new housing and then supported to sustain that housing. Most clients (79,400 clients, or about 81% of those who needed it) received assistance to sustain tenancy directly from the specialist homelessness agency.

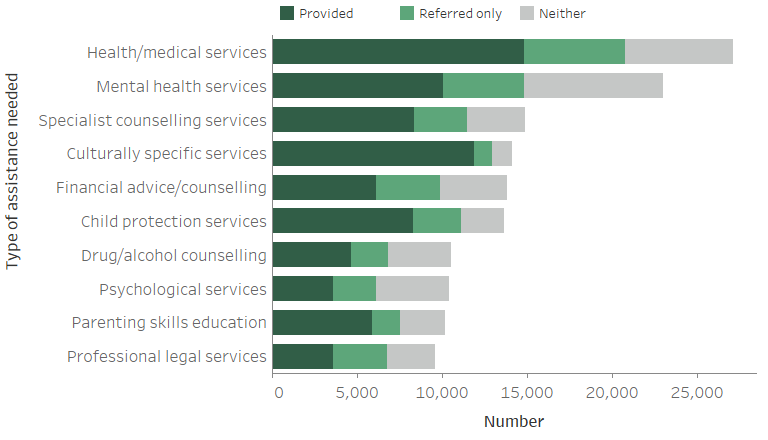

Specialised services

Specialised services refer to those services that require specific knowledge or skills and are usually undertaken by someone with qualifications to provide the particular service.

- Health/medical services were identified as needed by 1 in 10 clients (or just over 27,100) and were one of the services most often referred (22%) (Figure CLIENTS.11).

- There has been little change in the most common specialised services needed and provided over the past 5 years; for example, health/medical services, mental health services and specialist counselling remain the most commonly needed services.

Figure CLIENTS.11: Clients by need for specialised services and service provision status (top 10), 2018–19

Notes

- Excludes ‘Other specialised service’.

- ‘Neither’ indicates a service was neither provided nor referred.

- The specialised services group is a count of unique clients within all categories in the service and assistance group. A client may request multiple services and assistance types, therefore the sum of the categories is not equal to the group total.

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.18.

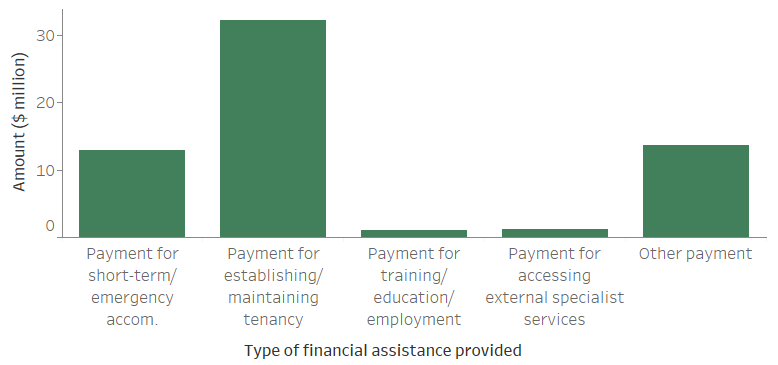

Financial assistance

$61.1 million in financial assistance was provided to clients in 2018–19.

Around $61.1 million in financial assistance was provided to clients in 2018–19 (Figure CLIENTS.12), a 16% increase from the $52.9 million provided in 2017–18 (not adjusted for inflation). This represents an average of $874 provided per client requesting financial assistance, and an increase from $794 in 2017–18 (not adjusted for inflation).

Around three-quarters of the financial assistance was used to assist clients with housing in 2018–19.

- Around $32.2 million (53%) of the financial assistance was used to assist clients to establish or maintain their existing tenancy.

- One-fifth of the financial assistance (21% or $12.9 million) was used to provide short-term or emergency accommodation.

Figure CLIENTS.12: Total amount of financial assistance provided to clients, by payment type, 2018–19

Note: Includes financial assistance, material aid, brokerage and vouchers provided to, or on behalf, of the client during the reporting period.

Source: Specialist Homelessness Services Collection 2018–19, Supplementary table CLIENTS.30.

Outcomes at the end of support

Outcomes presented here describe the change in clients’ housing situation between the start and end of support. Data is limited to clients who ceased receiving support during the financial year – meaning that their support periods had closed and they did not have ongoing support at the end of the year.

Many clients had long periods of support or even multiple support periods during 2018–19. They may have had a number of changes in their housing situation over the course of their support. These changes within the year are not reflected in the data presented here, rather the client situation at the start of their first period of support during 2018–19 is compared with the end of their last period of support in 2018–19.

Clients whose support period(s) both opened and closed in 2018–19 accounted for 75% of all clients (Figure CLIENTS.6). A proportion of these clients may have sought assistance prior to 2018–19, and may seek assistance again in future years.

Three aspects of a client’s housing situation are considered in their housing circumstances: dwelling type, housing tenure and the conditions of occupancy. See Technical notes for details on how each of these categories are derived.

- The number of clients who were known to be homeless at the start of support reduced when support ended: 1 in 3 clients (32% or over 59,500) were known to be homeless when support ended, down from 43% at the start of support (Table CLIENTS.2).

- The reduction in the proportion of clients who were homeless following support was due to decreases in the proportion of clients rough sleeping or with no shelter or living in improvised dwellings (from 10% to 6%) and in the proportion of clients living in a house, townhouse or flat as a ‘couch surfer’ with no tenure (from 17% to 12%).

- There was an increase in clients living in some form of tenure over the course of support, including an increase in the proportion of clients living in public or community housing from 15% (or 27,600 clients at the beginning of support) to 21% (or almost 39,000 clients at the end of support); and an increase in the proportion of clients living in private or other housing from 39% (or 73,900 clients at the beginning of support) to 44% (or 81,700 clients at the end of support).

These trends demonstrate that by the end of support, many clients have achieved or progressed towards a more positive housing solution. That is, clients ending support in public or community housing (renter or rent-free), private or other housing (renter or rent-free) or institutional settings had increased compared with the start of support.

| Housing situation | Beginning of support (number) | End of support (number) | Beginning of support (per cent) | End of support (per cent) |

|---|---|---|---|---|

| No shelter or improvised/inadequate dwelling | 19,104 | 11,037 | 10.0 | 5.9 |

| Short term temporary accommodation | 30,444 | 26,551 | 16.0 | 14.3 |

| House, townhouse or flat - couch surfer or with no tenure | 32,282 | 21,922 | 16.9 | 11.8 |

| Total homeless | 81,830 | 59,510 | 42.9 | 32.1 |

| Public or community housing - renter or rent free | 27,596 | 38,977 | 14.5 | 21.0 |

| Private or other housing - renter, rent free or owner | 73,896 | 81,657 | 38.7 | 44.0 |

| Institutional settings | 7,388 | 5,371 | 3.9 | 2.9 |

| Total at risk | 108,880 | 126,005 | 57.1 | 67.9 |

| Total clients with known housing situation | 190,710 | 185,515 | 100.0 | 100.0 |

| Not stated/other | 33,638 | 38,833 | ||

| Total clients | 224,348 | 224,348 |

Notes

- Percentages have been calculated using total number of clients as the denominator (less not stated/other).

- It is important to note that individual clients beginning support in one housing type need not necessarily be the same individuals ending support in that housing type.

- Not stated/other includes those clients whose housing situation at either the beginning or end of support was unknown.

Source: Specialist Homelessness Services Collection. Supplementary table CLIENTS.25.

Housing outcomes for homeless versus at risk clients

In general terms, for those clients who were known to be homeless at the start of support, agencies were able to assist those clients into temporary accommodation and sometimes into public or community housing or private or other housing. SHS agencies were also often successful in preventing those known to be at risk of homelessness from becoming homeless during support (Supplementary table CLIENTS.25, Interactive data visualisation).

- Over 8 in 10 (85% or 59,200) clients who were living in private or other housing were assisted to maintain their housing, while a further 6% (4,000) were assisted into public or community housing.

- Almost 9 in 10 (86% or 22,600) clients who were living in public or community housing were assisted to maintain their existing tenancy. A further 6% (1,600) were assisted into private or other housing and 1% (170) were in an institutional setting.

For clients with closed support in 2018–19 who were homeless on presentation to SHS agencies (Supplementary table CLIENTS.25, Interactive data visualisation).

- About 4 in 10 (38%) were assisted by agencies into housing; most were assisted into private or other housing (about 16,500) and a further 10,400 into public or community housing.

- More than 4 in 10 (43%) of those who were in short-term or emergency accommodation were assisted into housing; most were assisted into private or other housing (about 6,600) and a further 4,900 were assisted into public or community housing.

- The reduction in clients who were homeless following support was mostly due to reductions in the proportion of clients rough sleeping or with no shelter or living in improvised dwellings (from 10% to 6%) and in the proportion of clients living in a house, townhouse or flat as a ‘couch surfer’ with no tenure (from 17% to 12%).

Other outcomes for clients

Specialist homelessness agencies may support clients in a number of non-housing areas to reduce their vulnerability to homelessness. These include changes in educational enrolment status, labour force status and income.

Education

Education enrolment remained stable: 21% at the start of support and 22% at the end of support (Supplementary table CLIENTS.26). Of those who needed support for education or training assistance, 40% were enrolled at the start of support and 41% were enrolled at the end of support.

Employment

Employment increases following support. Of those with a need for employment assistance, 14% were employed at the start of support and 23% were employed at the end of the support (Supplementary table CLIENTS.27).

Income

Agencies assisted some clients receiving a government payment: 72% at the start of support and 78% at the end of support (Supplementary table CLIENTS.28). There was a reduction following support in those reporting no income from 13% to 8%), and the proportion waiting for government benefits halved from 7% to 3%.

Achievement of case management goals

Case management plans enable agency workers to assist a client to work towards agreed goals. In some cases, support periods are too short to allow for development of a case management plan; for example, when a client stays for a 24-hour period or less. In other cases, a client may decline a case management plan. Case management approaches can differ across SHS agencies and over time as state and territory policies and practices change.

- For those clients with closed support, 65% (or about 145,900 clients) had a case management plan—53% in their own right and 13% were part of another client’s case management plan, often as part of a family (Supplementary table CLIENTS.29). The proportion of clients with a case management plan was similar in 2017–18 (63%).

- Among those who had a plan in their own right, 70% achieved some of their case management goals, 25% achieved all their goals and 6% did not achieve any goals. The proportion of clients achieving all their goals was similar when compared with the previous year (24%).

- Of the 35% of clients whose support had ended and who did not have a case management plan, the most common reason given for not having one was that the service episode was too short (71%) while a further 10% did not agree to have a case management plan.